The key drivers of Indian’s Green Hydrogen growth are the decarbonization of the energy sector on the one hand, and energy security on the other. India has resource rich when it comes to solar and wind, thereby offering a huge upside potential for renewable energy generation, and there is also demand for Green Hydrogen in hard to abate energy intensive sectors of the economy. Beyond these, India’s strong and growing economy, and the expanding manufacturing sector offers India the chance to become a leader in Green Hydrogen Manufacturing technologies like electrolysers and fuel cells.

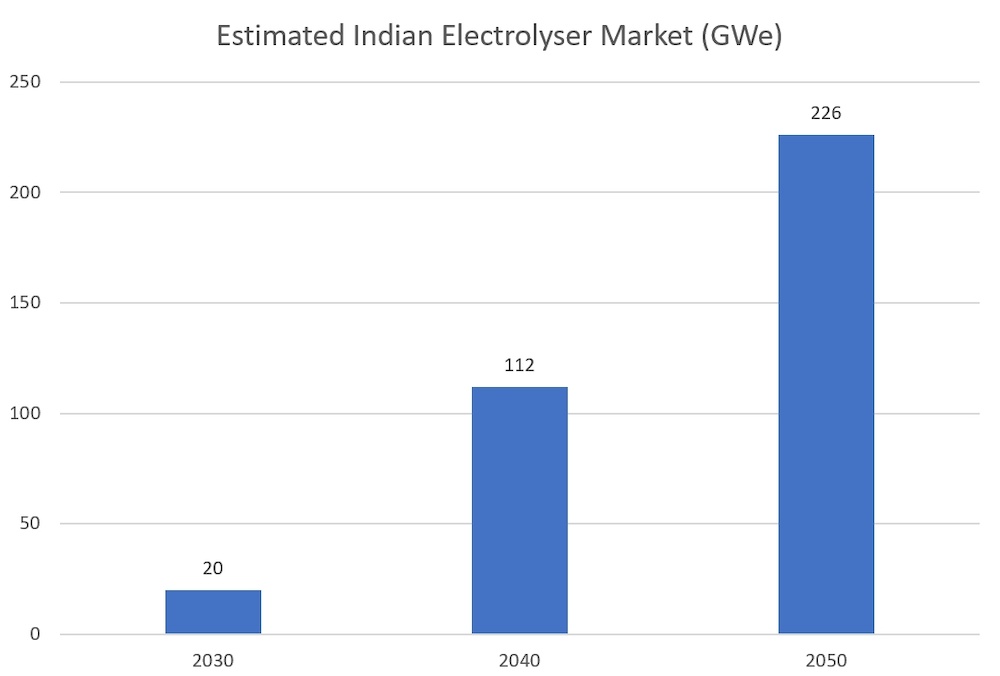

India’s Electrolyser Demand

According to the estimates of the NITI Aayog and RMI study , India’s domestic market for electrolysers could reach 226 GW, which translates to $31 billion by 2050. The shorter-term demand by 2030 is estimated to be 20 GW.

Source: NITI Aayog and RMI, 2022

As discussed in the previous part of the article series on Green Hydrogen, two types of electrolyser technologies dominate the market- alkaline and polymer electrolyte membrane (PEM) technologies. An electrolyser can be broadly divided into two systems of components

According to a cost analysis by IRENA that was reported in NITI Aayog report, 50 % of the total cost of both PEM and alkaline electrolysers are contributed by the stack. The other major cost of the total system cost of electrolysers is power supply, which accounts for another 20%-30% of the system cost. If the cost structure is expanded, 80% of the cost is made up of the stack, power supply and water circular system. If seawater is used for green hydrogen production, water desalination and water purification costs get added to the total cost of green hydrogen production.

When it comes to electrolysers, since rare-earth metals and precious metals like gold and platinum are essential components of PEM technology, it has higher share of material cost. According to the NITI Aayog report, since alkaline electrolysers use easily available nickel and has a simpler design, their cost is 50%-60% less than PEM electrolysers.

Status of Indian Electrolyser Market

India currently does not have a significant electrolyser manufacturing ecosystem. However, several Indian corporates have announced major plans to set up electrolyser manufacturing in India. According to Recharge news, Rystad Energy estimates India’s electrolyser capacity to ramp up to 8 GW by 2025, thereby making it a key player in the segment. This capacity includes seven factory projects by nine companies and three of these are joint ventures and three are solo investments. The companies who have made the announcements include Reliance Industries, Larsen and Toubro, H2e Power, Adani, Ohmium and Greenko. The details of the plants can be accessed here .

Conclusion

India requires a robust domestic electrolyser manufacturing base not only to meet the huge potential demand for Green Hydrogen, but also to ensure its energy security. With a high level of policy certainty and targeted incentives for domestic manufacturing, India will be in a position to meet it’s own demand as well as to become the major export hub for Green Hydrogen.